Rent is only part of the cost of renting a home. Before you sign a tenancy agreement in Hockley, it helps to work out the full picture, from your deposit to your monthly bills, so there are no surprises once you have moved in. Here is what to budget for and how to work out what you can realistically afford.

Start With the Rent Affordability Rule

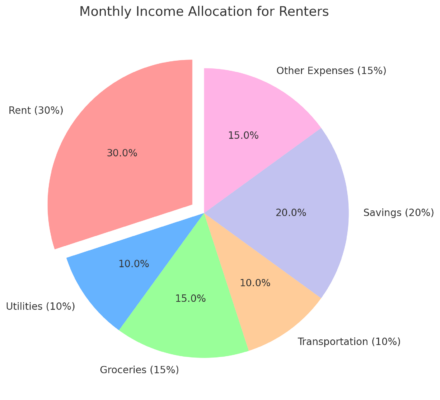

A common starting point is what is sometimes called the 30 per cent rule. This suggests spending no more than around 30 per cent of your income before tax on rent, to leave enough for bills, food and other costs without stretching your budget too thin. For example, if you earn £2,500 a month before tax, this would suggest a rent of up to around £750 a month.

This is only a guide rather than a hard limit, and plenty of tenants spend more than this depending on their circumstances, particularly in areas with strong demand. The important thing is to be honest with yourself about what you can afford once every other cost is accounted for, rather than working backwards from a property you have already fallen for.

What You Will Pay Before You Move In

When you find a property you want to rent, there are usually two payments to make before you get the keys.

Holding deposit. This reserves the property while referencing is carried out and is capped by law at no more than one week’s rent. It should be refunded or put towards your first month’s rent once the tenancy begins, as long as your application goes ahead as planned.

Tenancy deposit. Once your tenancy is confirmed, you will need to pay a deposit, which by law is capped at five weeks’ rent for most tenancies. This must be placed into a government-approved deposit protection scheme within 30 days, and you should be given written confirmation of which scheme is being used.

Letting agents are not permitted to charge tenants extra fees for viewings, credit checks or setting up the tenancy itself under the Tenant Fees Act, so these two payments, along with your rent, should be the only costs an agent asks you for.

Ongoing Monthly Costs

Once you have moved in, your rent is usually just one line in a wider monthly budget. Other regular costs to plan for include:

- Council tax. The amount depends on the property’s council tax band and whether you qualify for any discounts, such as living alone.

- Gas and electricity. Costs vary depending on the size of the property and how it is heated, and are separate from your rent unless your agreement states otherwise.

- Water. Usually billed separately by the local water supplier.

- Broadband and TV. Worth checking what is available at the property before you commit to a contract.

- Contents insurance. Your landlord’s insurance covers the building itself, not your belongings, so this is worth budgeting for separately.

Some tenancies are advertised as “bills included,” which can make budgeting simpler, but always confirm exactly which bills are covered and which, if any, you would still need to arrange yourself.

Moving Costs Add Up Too

It is easy to focus on rent and deposits and forget the practical costs of actually moving house. Removal vans, cleaning, redirecting your post and even the small cost of updating your address with your bank and employer can add up. Building a small buffer into your budget for the first month or two of a new tenancy is generally sensible, since unexpected costs are common when you are settling into anywhere new.

Checking You Can Really Afford It

Before committing to a property, it is worth listing your income and outgoings properly rather than estimating. Include your take-home pay, then set out fixed costs such as rent, council tax and any existing debt repayments, followed by variable costs like food, transport and everyday spending. MoneyHelper’s free budget planner tool is a useful way to work through this in detail and see what you have left over each month before you commit to a tenancy.

If your budget is tight, it is worth checking whether you might be entitled to help with housing costs through Universal Credit, and building in an emergency fund if you can, since even a well-planned budget can be knocked off course by an unexpected bill or a change in income.

Getting the Right Property for Your Budget

Once you know what you can genuinely afford each month, it becomes much easier to search for properties that actually fit, rather than stretching for something at the top of your budget and hoping for the best. Hockley offers a good range of property types and price points, from flats and terraced cottages in the village centre to larger family homes on the surrounding estates, so there is usually something to suit most budgets.

The lettings team at Williams & Donovan’s Hockley branch can talk you through current rental prices in the area and help you find a property that matches both your needs and your budget. If you are ready to start looking for a rental home, get in touch with Williams & Donovan in Hockley for advice on what is currently available.