Living between two countries financially is more common than it used to be, and the tax questions that come with it are rarely straightforward. Many overseas Pakistanis in the UK assume that because they pay tax here, their obligations abroad are either covered or irrelevant. That assumption creates real risk. Getting proper overseas tax advice is not about paying more.it is about understanding what applies to your situation before HMRC or the Federal Board of Revenue in Pakistan decides to ask questions you are not prepared to answer.

This guide works through the most common concerns: residency, property income, double taxation, remittances, foreign bank accounts, and what happens if something was missed in a previous tax year.

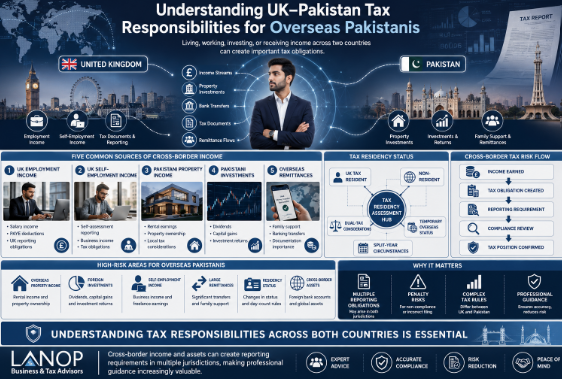

Why Cross-Border Tax Compliance Has Become More Important?

The financial ties between the UK Pakistani community and Pakistan are substantial and varied. Some people own property in Lahore or Karachi that generates rental income. Others send regular money to support parents. Many have inherited land or assets. Some hold savings in Pakistani banks or investments in local funds.

None of these arrangements are unusual, and none of them are automatically problematic. What has changed is visibility.

International financial information sharing has expanded considerably in recent years. Under the Common Reporting Standard, financial institutions in many countries including Pakistan share account data with foreign tax authorities. HMRC has invested in cross-border compliance. Digital tax administration has made it significantly easier for authorities to cross-reference what taxpayers declare against what financial institutions report globally.

The honest message here is simple: income and assets held overseas are not as invisible to UK tax authorities as many people believe. Reporting obligations exist, and penalties for non-compliance apply regardless of whether the non-disclosure was intentional.

Understanding Where You Are Tax Resident

Tax residency is not the same as citizenship, and the distinction matters enormously.

A British Pakistani holding both nationalities does not become non-resident in the UK by virtue of their Pakistani citizenship. UK tax residency is determined by the Statutory Residence Test, which considers how many days someone spends in the UK, the nature of their ties here work, family, accommodation, and other connections and their overall pattern of presence. Most people living and working in the UK full-time will be UK tax resident, regardless of where they were born or hold citizenship.

Pakistan has its own residency rules. A person is generally considered a non-resident Pakistani if they spend fewer than 183 days in Pakistan in a tax year and do not have an ordinary place of residence there. Non-resident Pakistanis are typically taxed only on Pakistan-source income arising from assets or activities within Pakistan rather than their worldwide income.

Dual residency situations do occur and they complicate things further. If both countries claim tax residency simultaneously, the UK-Pakistan Double Taxation Agreement contains tie-breaker provisions to determine which country’s rules take precedence.

Do Overseas Pakistanis Need to Pay Tax in Pakistan?

Non-resident status in Pakistan does not eliminate all obligations there.

Rental income from a property in Pakistan is taxable in Pakistan, regardless of where the owner lives. Business income generated from Pakistani operations, dividends from Pakistani companies, and gains from selling property within Pakistan may all trigger Pakistani tax obligations. The fact that the recipient lives in Birmingham rather than Karachi does not change where the income arises.

Whether a tax return needs to be filed in Pakistan depends on the nature and amount of that income. Rental income above certain thresholds, for instance, requires filing through the FBR’s online system. Failing to file when required creates a record of non-compliance that can complicate future dealings property transactions, for example, often require a clean tax filing history.

The practical point is this: having Pakistani source income does not automatically create a major tax burden, but it does create a reporting responsibility that is worth taking seriously.

Can You Be Taxed in Both Countries?

This is the question almost everyone asks first, usually with considerable anxiety.

Reporting income in two countries is not the same as paying tax twice. The UK-Pakistan Double Taxation Agreement, which has been in force for several decades, exists precisely to prevent the same income being taxed twice. Under the treaty, where income is taxed in one country, the other country typically gives credit for that tax against its own liability. The mechanism varies depending on the type of income, but the principle is consistent: you should not end up paying full tax rates in both jurisdictions on the same sum.

A practical example makes this clearer. Suppose a UK resident owns a flat in Lahore that generates rental income of £6,000 per year. Pakistan may charge withholding tax on that rental income at source. When that income is then declared in the UK which it must be, as UK residents pay tax on worldwide income the UK tax liability is calculated, and credit is given for the Pakistani tax already paid. If Pakistani tax covers the full UK liability, no additional UK tax is due. If the UK rate is higher, the difference is payable to HMRC. In no scenario should the total tax exceed the higher of the two rates.

Can HMRC See Income and Assets Held in Pakistan?

Directly: they may already have data on Pakistani financial accounts, depending on the institution and the reporting standards it follows. Pakistan is part of international transparency initiatives, and data exchange between tax authorities has expanded considerably. That does not mean every rupee in a savings account in Lahore automatically lands on an HMRC screen, but it does mean that the assumption of complete invisibility is no longer safe.

Foreign bank account interest must be declared on a UK Self Assessment return if the total untaxed income exceeds the personal savings allowance threshold. Dividends from Pakistani company shareholdings, returns from Pakistani mutual funds, and interest from National Savings certificates are all income that a UK-resident taxpayer is required to report.

The common misconception that if Pakistani tax was deducted at source, there is nothing else to do is incorrect. The obligation to declare the income in the UK exists separately from whether tax was paid there. Disclosure is almost always a better outcome than later discovery, both financially (penalties are lower, interest stops accruing) and practically.

Owning Property in Pakistan While Living in the UK

Property is where most of the complexity concentrates for overseas Pakistanis.

Rental income from Pakistani property must be reported to HMRC annually through Self Assessment. The currency needs converting to sterling using an acceptable exchange rate. Allowable expenses, repairs, management costs, agent fees can reduce the taxable figure in much the same way as UK rental properties.

Selling a property in Pakistan introduces a different set of considerations. Capital gains on the sale of overseas property are generally subject to UK Capital Gains Tax for UK residents, though the rate and any available reliefs depend on the circumstances including how long the property was held and whether it was ever a main residence. Pakistani Capital Gains Tax may also apply, and the double taxation agreement provides the mechanism for calculating the net liability across both countries.

Inherited property is a situation that catches people off guard. Receiving an inherited property in Pakistan does not itself trigger UK tax, but once that property generates income through rent or is sold, the usual reporting rules apply. Many people inherit a share of a family home, never formalise the ownership, and find years later that undeclared rental income has accumulated alongside it.

Jointly owned family property is common and creates its own issues around income allocation and documentation.

Are Remittances Between the UK and Pakistan Taxable?

Sending money to family members in Pakistan to support parents, contribute to a sibling’s household, or help with medical costs is not taxable in the UK. Gifts of money to family members are not treated as income for UK tax purposes, and there is no specific remittance limit that triggers automatic tax liability.

The complications arise elsewhere. Large bank transfers attract scrutiny from financial institutions under anti-money laundering regulations. Banks may ask for source-of-funds documentation. HMRC may, in certain circumstances, question the origin of transferred funds if they appear on a tax return or compliance check. Keeping a clear record of where transferred money came from savings, salary, inheritance is not an obligation in most cases, but it is sensible practice that prevents unnecessary difficulty later.

Receiving money from Pakistan into a UK account works the same way in principle. Money transferred from Pakistani savings, or a family gift, is generally not UK taxable income. What matters is the underlying source of the money, not the transfer itself.

What Happens If You Forgot to Declare Foreign Income?

This is a concern worth addressing without drama. Errors and omissions in tax returns happen regularly, often because of genuine misunderstanding rather than deliberate concealment, and HMRC has established mechanisms for correction.

The most common reasons overseas income goes unreported are: not knowing it was required, receiving incorrect advice, or misunderstanding residency status. These are understandable mistakes. They do not make the resulting non-compliance acceptable, but they do affect how HMRC treats the situation when it comes to light.

Correcting past errors proactively rather than waiting for HMRC to raise the issue almost always produces a better outcome. Penalties for unprompted disclosure are lower than for cases where HMRC discovers the omission independently. Interest stops running from the date the correction is made. The process exists specifically for situations like this, and using it is generally far preferable to hoping the issue never surfaces.

The Most Common Tax Mistakes Overseas Pakistanis Make

Several errors appear consistently when cross-border tax situations are reviewed.

Assuming tax paid in Pakistan satisfies all UK obligations is the most common and most costly. It does not. UK residents report worldwide income regardless of where it arises or where it was already taxed.

Ignoring rental income from Pakistani property on the basis that it is small or that family members manage it informally does not change the reporting requirement. The income exists; it must be declared.

Missing Self Assessment deadlines for overseas income creates surcharges and interest on top of the underlying liability. Year-end is not always obvious for people used to PAYING employment, but once overseas income creates a filing requirement, that obligation continues annually until circumstances change.

Not reporting foreign bank interest, assuming that the small amounts involved will not be noticed, is a mistake that has become riskier as information sharing has improved.

A Cross-Border Tax Compliance Checklist

A quick reference for keeping obligations in order across both countries:

Residency: Confirm UK residency status under the Statutory Residence Test. Understand non-resident Pakistani status and its implications.

Income sources: List all income arising in Pakistan rental, business, savings interest, dividends. Convert to sterling and check reporting thresholds.

Property: Confirm rental income is declared annually. Understand capital gains implications before selling. Record inherited property and its subsequent income.

Bank accounts: Note all Pakistani bank accounts and the interest earned. Check whether any accounts fall under automatic information exchange.

Remittances: Retain records of large transfers showing source of funds. Keep evidence that regular family payments come from taxed income.

Tax returns: File UK Self Assessment on time if overseas income exists. Check Pakistani filing requirements for Pakistan-source income.

Professional review: Have a qualified adviser review the position if circumstances have changed, property has been acquired or sold, or income sources have increased.

When Professional Help Is Worth Considering?

Most people managing straightforward Pakistani rental income alongside UK employment can handle their position with reasonable care and a correctly filed Self Assessment. The situation becomes more complex quickly once multiple income streams are involved, property has been sold, significant assets have been inherited, or there is uncertainty about residency status.

Proper overseas tax advice becomes particularly valuable when reviewing historic returns when someone suspects they may have missed a reporting obligation in previous years and wants to correct the position before it becomes a larger problem. In those cases, the difference between acting promptly with professional guidance and hoping nothing surfaces can be measured directly in penalties and interest.

Frequently Asked Questions

Do overseas Pakistanis living in the UK need to file a tax return in Pakistan?

It depends on whether you have Pakistan-source income. Non-resident Pakistanis are taxed only on income arising within Pakistan rental income, business profits, dividends, or property sale proceeds. If that income exceeds the FBR filing threshold, a Pakistani return is required regardless of where you live. Non-residency narrows your obligations there, it does not eliminate them.

What happens if I have been receiving rental income from a Pakistani property but never declared it to HMRC?

It is correctable. UK residents must declare worldwide rental income through Self Assessment. If that was missed, HMRC’s voluntary disclosure process exists precisely for this situation. Acting proactively results in significantly lower penalties than waiting for HMRC to raise the issue. The sooner the correction is made, the less interest and penalty accumulates.

Is the money I send to my parents in Pakistan treated as taxable income by HMRC?

No. Family remittances and gifts sent abroad are not taxable in the UK for either party. Where questions arise is around the source of the funds.if large transfers originate from income with an unclear origin, banks may ask for documentation. Keeping basic records of where transferred funds came from is sensible precaution.

If I sell a property in Pakistan, do I owe tax in the UK as well as Pakistan?

Potentially yes. UK residents are subject to Capital Gains Tax on overseas property disposals. Pakistani Capital Gains Tax may also apply to the same transaction. The UK-Pakistan Double Taxation Agreement provides relief so that tax paid in Pakistan is credited against the UK liability, preventing the same gain from being taxed twice in full.

How far back can HMRC investigate unreported overseas income?

It depends on the nature of the non-disclosure. Genuine errors allow HMRC to go back four years. Careless behaviour extends that to six years. Deliberate non-disclosure can reach back twenty years. This is one of the strongest arguments for correcting historic omissions early; the longer the gap, the more years of tax, interest, and penalties can potentially be in scope.

Conclusion

Cross-border tax compliance for overseas Pakistanis living in the UK is not as complicated as it sometimes feels, but it does require attention. UK residents pay tax on worldwide income, report foreign assets where required, and claim treaty relief to avoid double taxation. Getting the basics right from the start is almost always easier and less expensive than correcting a problem after it has grown.

Lanop Business and Taax Advisors works with overseas Pakistanis who have property in Pakistan, foreign savings, family remittances, or historic reporting gaps they want to resolve. From Self Assessment returns that correctly account for Pakistani rental income, to capital gains advice when a Pakistani property is sold, to voluntary disclosures that correct past omissions we handle the detail across both jurisdictions so you do not have to piece it together alone.

If your cross-border tax position needs a proper review, Lanop Business and Tax Advisors is the right place to start.